Long-Term Care Insurance

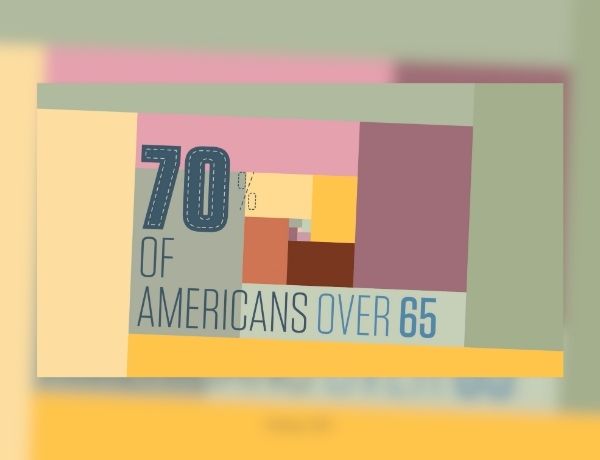

Addressing the potential risks of long-term care (LTC) or "extended care" expenses may be one of the biggest financial challenges for individuals who are developing a retirement strategy. Extended care is not a single activity. It refers to a variety of medical and non–medical services needed by those who have a chronic illness or disability – most commonly associated with aging.

Extended-care coverage can be complex. It is important to have good understanding of the topic and a list of questions to ask that may help you better understand the costs and benefits of these policies.